Home Loan Interest Rate Updates 2026: Key Factors Influencing Housing Loan Costs this Year

Jun 09, 2026

NewsVoir

Pune (Maharashtra) [India], June 9: Home loan interest rates in India are shaped by the RBI repo rate, your CIBIL Score, and loan tenure. Use an EMI calculator to estimate costs before you apply.

In summary

Home loan interest rates in 2026 are influenced by a mix of macroeconomic signals and your personal financial profile. The RBI held its repo rate at 5.25% in June 2026, which affects how lenders price their products. Your CIBIL Score, income stability, loan amount, and the property you choose all play a role in the final rate you're offered.

On a Rs. 50 lakh loan over 20 years, a difference of just 1% in your interest rate changes your EMI by over Rs. 3,000 per month - and your total interest outgo by over Rs. 7 lakh. Using an EMI calculator for home loan planning helps you see this clearly before you commit. This article covers what's moving rates this year, how to assess your own position, and how to compare options with numbers.

What's affecting home loan interest rates in 2026?

Home loan interest rates don't move in isolation. They shift with broader monetary policy, inflation trends, and banking system conditions. Understanding these can help you time your decision better.

The repo rate signal

Per the RBI's Monetary Policy Committee announcement on 5 June 2026, the policy repo rate was kept unchanged at 5.25%. The MPC voted unanimously to maintain this rate and continued with its neutral stance. For borrowers, a stable repo rate means lenders have less pressure to revise rates sharply in either direction in the short term.

Inflation and liquidity

When inflation stays within the RBI's target band of 4%, lenders can hold rates steady. If inflation rises, rate hikes follow, which pushes up home loan interest rates across the board. Banking system liquidity also matters: tighter liquidity typically means higher short-term borrowing costs for banks, which can filter through to retail loan rates.

External benchmark-linked rates

Since 2019, the RBI has required that floating-rate home loans be linked to an external benchmark such as the repo rate. This means rate changes by the RBI now pass through to borrowers more directly than before. It's worth checking whether your lender offers repo-linked rates so you can benefit when rates ease.

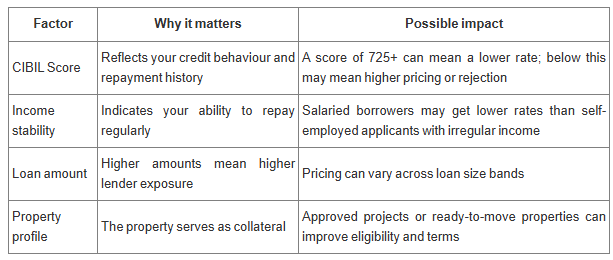

Which factors can affect your home loan interest rate?

Your personal financial profile has a direct bearing on the rate you're offered. Lenders assess risk, and a stronger profile generally means a lower rate.

A borrower with a CIBIL Score of 780 could be offered a better rate than one with a score of 700 on a Rs. 65 lakh loan over 20 years, and that difference compounds significantly. It's worth cleaning up any credit report errors before applying.

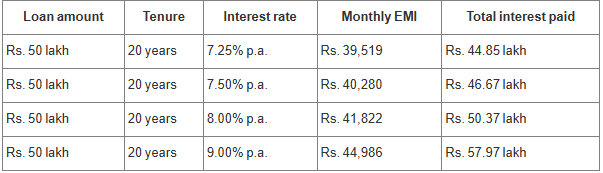

How much difference can a small rate change make?

This is where the numbers make the case. Many borrowers focus on the loan amount but underestimate how much the rate itself affects total repayment.

Even a 0.25% difference in your rate matters at higher loan amounts:

The difference is roughly Rs. 1.82 lakh over the loan's full term. That's money you could use for other goals. This comparison shows why securing the best possible rate from the start matters far more than it might seem.

How can an EMI calculator for home loan help you plan?

An EMI calculator for home loan estimates your monthly repayment using three inputs:

- Loan amount you plan to borrow

- Expected interest rate (or a range you want to compare)

- Loan tenure in years

It instantly gives you clarity before you speak to any lender by showing you estimates for:

- Your monthly EMI figure

- Total interest payable over the full tenure

- Total repayment amount (principal + interest)

- An amortisation schedule showing how much goes to principal and interest each month

The Bajaj Finance Home Loan EMI Calculator lets you adjust all three inputs and see results instantly. This helps you compare a 15-year versus a 20-year tenure side by side, without any paperwork or phone calls.

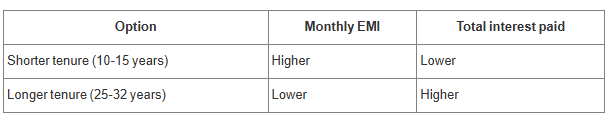

Should you choose a shorter or longer loan tenure?

Tenure is one of the most practical decisions you'll make. There's no universal right answer; it depends on your monthly cash flow and your appetite for total interest cost.

If your income allows for a higher EMI comfortably, a shorter tenure saves you more, as the table shows. If you need breathing room in your monthly budget, a longer tenure keeps payments manageable. You can always make part-prepayments later to reduce the outstanding principal and, effectively, shorten your loan.

What can you do if interest rates rise?

Rate increases aren't always avoidable, but you can manage their impact with a few deliberate steps.

- Improve your CIBIL Score before applying: every point above 725 can work in your favour

- Increase your down payment to reduce the loan amount and your risk profile

- Make periodic part-prepayments to reduce the principal and limit future interest accrual

- Review balance transfer options if another lender offers a materially better rate

- Recalculate your EMI using a calculator periodically to track how much you still owe and how long remains

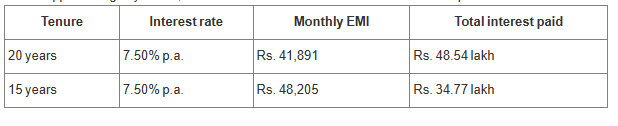

Scenario: Pritha is 34, works as a salaried software professional in Pune, and earns Rs. 20 lakh per year. Her CIBIL Score is 760. She's identified a property worth Rs. 65 lakh and plans to pay 20% (Rs. 13 lakh) as a down payment, bringing her loan requirement to Rs. 52 lakh.

Before approaching any lender, she used an EMI calculator for home loan to compare two scenarios:

The Rs. 6,314 monthly difference showed her she could afford the 15-year option within her budget. She chose it and will pay Rs. 13.77 lakh less in interest over the term.

When should you review a home loan balance transfer?

If you took a home loan two or more years ago at a higher rate, it may be worth reviewing whether a balance transfer makes financial sense. The savings can be material, especially in the early years of a loan when interest makes up the larger portion of each EMI.

A balance transfer moves your outstanding principal to a new lender at a lower rate. It's not a new loan; it's a refinancing of what you already owe.

Bajaj Finance offers home loan balance transfer rates starting at 7.30%* p.a. If your current rate is above this, the difference over the remaining tenure could add up to significant savings. Additionally, eligible balance transfer customers can apply for a top-up loan of up to Rs. 1 crore*, which can be used for home improvements, medical costs, or other needs with end-use flexibility.

How to apply for a Bajaj Finance Home Loan?

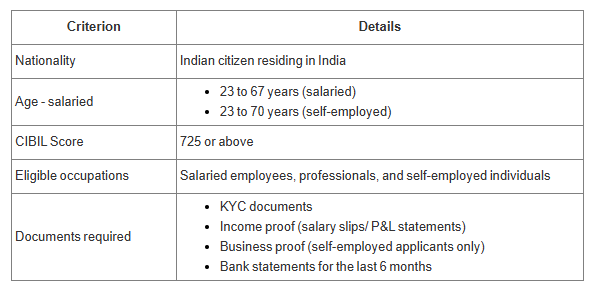

Who can apply?

To apply for a Bajaj Finance home loan, you must meet the following eligibility criteria. Checking your eligibility before applying saves time and helps you prepare the right documents.

Step-by-step process for online application

- Click on the 'APPLY' button on the Bajaj Finance Home Loan page.

- Enter your full name, mobile number, and employment type.

- Select the type of loan you wish to apply for.

- Generate and submit your OTP to verify your phone number.

- Enter additional details, including your monthly income, required loan amount, and whether you have identified a property.

- Enter your date of birth, PAN, and other details as requested based on your occupation type.

- Click the 'SUBMIT' button.

- Your application is submitted. A Bajaj Finance representative will contact you to guide you through the next steps.

Home loan interest rates in 2026 are shaped by the RBI's monetary stance, inflation signals, and your own financial profile. Understanding what drives your rate, and by how much, puts you in a stronger position before you walk into any application. Use an EMI calculator for home loan to run through different loan amounts, tenures, and rates so you know exactly what you're committing to each month. Affordability isn't just about what you can borrow; it's about what you can repay comfortably over time. Explore Bajaj Finance Home Loan options, compare repayment scenarios, and estimate your EMIs before making a borrowing decision.

(ADVERTORIAL DISCLAIMER: The above press release has been provided by NewsVoir. ANI will not be responsible in any way for the content of the same.)